Consumer Duty is not a single issue affecting one part of the company. It is a holistic, whole of company approach to managing the most significant regulatory obligation of modern times. It runs through file reviews, financial promotions, vulnerable customer records, monitoring and the management information that ties them together.

What It Does

My Compliance Centre supports the consumer duty programme, so you can evidence good customer outcomes rather than just assert them. Consumer Duty changed what the FCA expects. Firms have to deliver good outcomes across products and services, price and value, consumer understanding and consumer support – and evidence that they are doing it. That evidence does not sit in one place. It comes from the file reviews, the financial promotions sign-off, the vulnerable customer records, the monitoring and the management information already produced across the firm. The hard part is rarely doing the work. It is holding it together in a form your Board and the FCA can rely on.

Key Capabilities

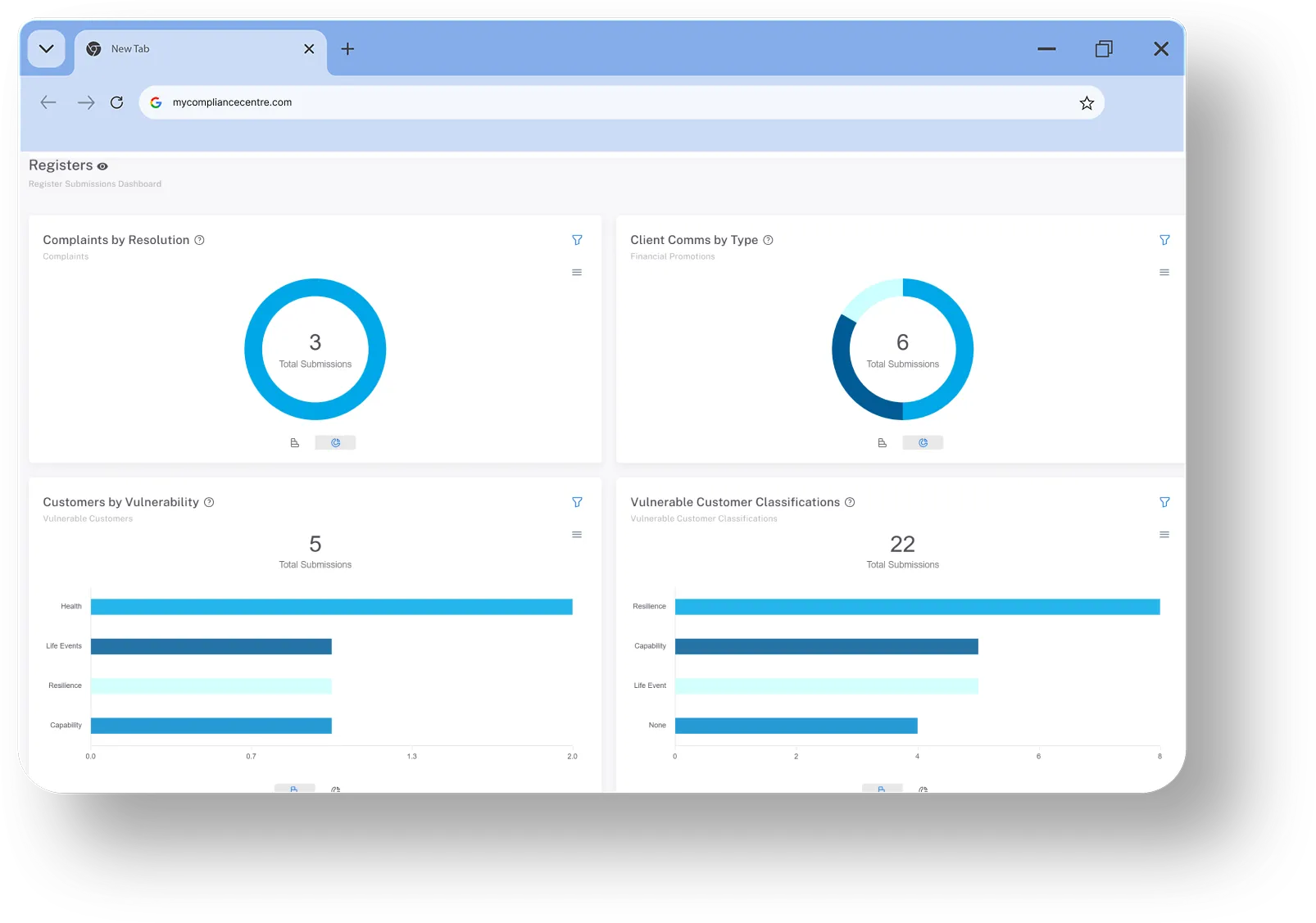

File reviews – FileChecker structures your file reviews and scores them against criteria you set, including whether the customer got the right outcome, not just whether the file is complete. Findings are recorded, remediation is tracked to closure, and the trends show whether outcomes are improving.

Financial promotions – Every promotion taken through submission, review, approval or return in one process, with a full record of who approved what and when. The evidence that your communications are fair, clear and not misleading is kept as you go, not reconstructed when someone asks for it.

Vulnerable customers – records held in Register Vault, with a workflow for recording, reviewing and escalating. You can show that vulnerability is being identified and that those customers are getting the right support across the whole customer base, rather than the cases you happen to recall.

Compliance monitoring – Your monitoring programme set up to test whether good outcomes are actually being delivered, not assumed. Ownership is assigned, findings are tracked to resolution, and the results feed straight into your management information.

Management information – Consumer Duty stands or falls on the MI behind it. The platform pulls together the output of file reviews, monitoring, complaints and vulnerable customer records into management information your Board can act on – the evidence base for your annual assessment, built as the work happens.

Governance and the annual board report – Board and committee packs, minutes, actions and attendance recorded and evidenced, including the work of your Consumer Duty champion. When the annual board report is due, the supporting evidence is already in the system, not assembled from scratch.

Regulatory change – Track the FCA’s continuing Consumer Duty expectations – Dear CEO letters, reviews and guidance – assign the actions they create, and evidence your firm’s response in a structured, auditable way.

What This Means in Practice

You are not buying a Consumer Duty button. You are putting the evidence of good outcomes – file reviews, promotions, vulnerable customer support, monitoring and MI – in one place, kept current as the work happens. When your Board signs off the annual report, or the FCA asks how you know your customers are getting good outcomes, the answer is in the system.

Frequently Asked Questions

Firms evidence the Consumer Duty by pulling together the records that show good customer outcomes – file reviews, financial promotions, vulnerable customer support, compliance monitoring and management information – and keeping them current, not assembled once a year. My Compliance Centre brings those records into one place, so the evidence is ready when your Board or the FCA asks.

The annual board report needs to show how the firm is delivering good outcomes across the four outcomes – products and services, price and value, consumer understanding and consumer support – backed by management information and the actions taken where outcomes fall short. The platform pulls that MI together and holds the report, its actions and oversight in the governance module.

You evidence it by recording how vulnerability is identified, what support each customer is given, and the outcome they received – across the whole customer base, with an audit trail, not just the cases you recall. My Compliance Centre holds this in Register Vault, with a workflow for recording, reviewing and escalating.

Consumer Duty MI should show whether good outcomes are actually being delivered, not just activity volumes – drawn from file review results, monitoring findings, complaints and vulnerable customer data. The platform builds that MI as the work happens, so the evidence base for your annual assessment is always current.

No single module delivers Consumer Duty, because it runs across the whole business – and you should be wary of any product that claims otherwise. What software can do is bring the evidence from the areas that matter – file reviews, financial promotions, vulnerable customers, monitoring, MI and governance – into one place. That is what My Compliance Centre does.

You can record the work on spreadsheets, but they hold data without joining it up, so producing current evidence for the board report or an FCA request is slow and gaps are easy to miss. A platform keeps the evidence live and in one place, ready when you need it.

Let us show you how My Compliance Centre can make a difference to your risk and compliance management

Fill in your details and we will give you a call to arrange a demo. Alternatively, call us on +44 (0)20 8017 8273 or email info@mycompliancecentre.com.